A deep dive into the infrastructure, tools, and dynamics shaping prediction markets (Polymarket & Kalshi)

Table of contents:

- The Four Layer Stack of Prediction Markets

- Ecosystem Landscape

- Analysis & Insights

- Value Capture

- Prediction Markets 101: A Practical Q&A

- What are Prediction Markets?

- How are markets/bets created on prediction markets?

- What types of markets are typically available on Prediction platforms?

- How does trading actually work on prediction markets?

- How do Polymarket and Kalshi differ?

- Are prediction markets always efficient, and why do price imbalances exist?

In the past two years, prediction markets (mainly Polymarket and Kalshi) have risen in popularity. These platforms enable people to bet on the outcome of diverse real world events such as presidential elections or Fed rate cuts.

For readers who are newer to the field, I added a practical Q&A section at the end covering the questions I asked myself when I started this deep dive.

These prediction markets sound very similar to traditional betting, so what actually makes them different?

- First, prices instead of fixed odds. A market is created around a real world question, like an election result or something more silly such as “Will Elon Musk publish 456 tweets by the end of December” (one of the most popular markets on Polymarket). Each possible outcome is represented by a contract that pays out a fixed amount if it happens. People buy or sell these contracts based on their beliefs. If more people think an outcome is likely, demand increases and the price goes up. When the event is resolved, winning contracts pay out and losing ones become worthless.

- Second, there is no bookmaker setting the odds. In classic betting, odds are set and controlled by a bookmaker behind closed doors. On prediction markets, prices move continuously based on supply and demand, much like in financial markets. And this is a major difference because unlike traditional betting websites, prediction markets let you exit a position before the event is resolved. If you buy a contract at a given price and, weeks later, the market price rises, you can sell that contract early and lock in a profit without waiting for the final outcome.

- Third, closed versus open systems. Traditional betting platforms are relatively opaque when it comes to transactions and user activity (you can have access to some data, but it’s very limited and controlled). On blockchain based prediction markets like Polymarket, every trade, position, and wallet interaction is visible. This openness allows anyone to analyze activity, build tools, or automate strategies. Instead of betting against a house, participants are effectively trading against each other, and the price itself becomes a signal of collective belief.

It may sound like technical differences only, but it actually enables behaviors, trading strategies, and tools that are unique to prediction markets and impossible on traditional betting platforms. These “emergent behaviors” are giving birth to a whole ecosystem of tools, software and protocols that is getting built around the exchanges themselves.

This is what I’m exploring in the rest of this article.

The Four Layer Stack of Prediction Markets

Before diving into the prediction markets ecosystem and its analysis, I want to introduce the framework I use to break it down into a four layer stack.

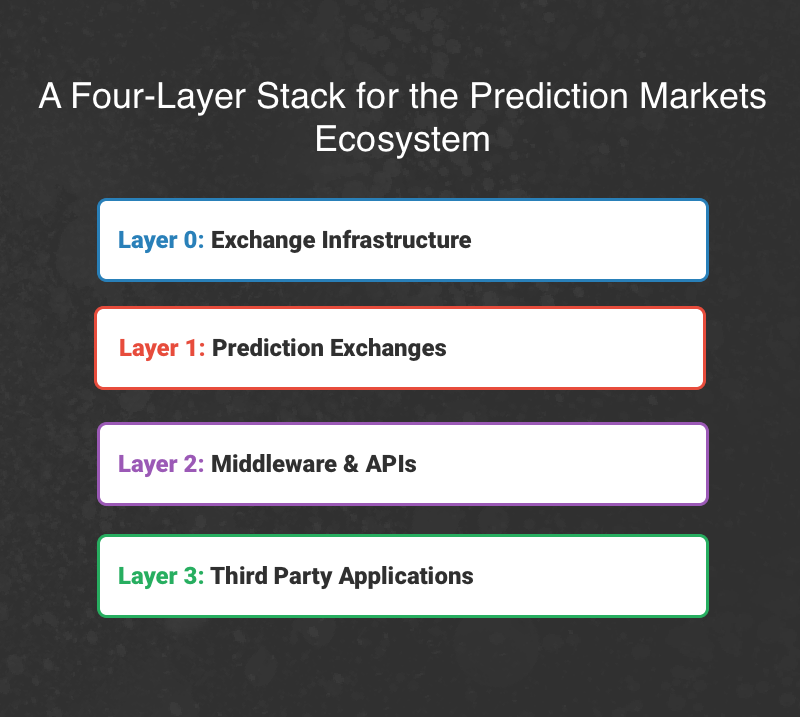

Layer 0: Exchange Infrastructure

The infrastructure on which prediction exchanges are built.

- Transaction and smart contracts: Infrastructure that enables exchanges like Polymarket and Kalshi to execute transactions. Examples include Solana and Polygon.

- Verification layer: Tools that verify off chain data and resolve disputes. Example: UMA.

Layer 1: Exchanges

The exchanges themselves, where markets are created and where people place their bets. Examples include Polymarket and Kalshi.

Layer 2: Middleware and APIs

The middleware and APIs built on top of the exchanges that allow third party developers and businesses to interact with prediction markets or build applications on top of them.

- Data providers: API providers that help developers integrate prediction market data more easily into their products. Example: Dome.

- Execution & Integration Infrastructure: APIs and middleware that abstract the complexity of prediction markets by handling connectivity, smart contracts, and core interactions, allowing developers to build products without dealing directly with on chain mechanics. Example: Azuro.

Layer 3: Applications

Third party applications built on top of prediction exchanges and directly facing end users or businesses.

- Analytics tools: Software that helps visualize live and historical data to support betting decisions. Example: Polywhaler.

- Trading terminals and bots: Tools designed to make trading easier, including multi exchange trading and portfolio management. Example: Polymtrade.

- Finance: Products that help users manage the capital they have placed on these exchanges, whether to create funds or for asset management, allocation, or lending. Example: Gondor.

Now that we have this four layer framework in mind, let’s explore the protocols, startups, and indie hacker projects that are making it.

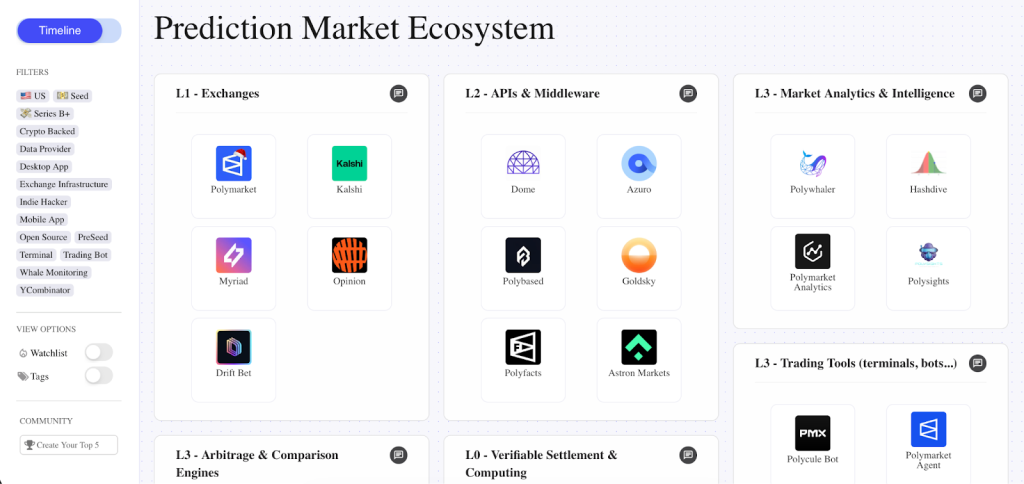

Ecosystem Landscape

Below you will find an interactive landscape that lists more than 60 startups, tools, and protocols. Simply click on the company cards to see more information, or use the left sidebar to filter the landscape according to your preferences.

Analysis & Insights

Here are my main takeaways from researching the prediction markets ecosystem:

Ecosystem Structure

- Prediction markets: The “financialization of information.” At the heart of this trend lies the financialization of information. When you step back and look at history, financialization has been a recurring trend in human societies. From the emergence of commerce (the financialization of barter) to wages (the financialization of labor), land ownership (the financialization of lands), insurances (the financialization of risk) and more recently stock markets. The rise of prediction markets feels like a continuation of this trajectory in an increasingly digital world.

- Lipstick on a pig: Is it just online betting? Some argue (and I think it is a fair point) that there is nothing fundamentally new compared to traditional betting platforms. For decades, people have been able to bet on trivial events, such as the color of the British Queen’s hat. So what is actually different here? I believe that the key distinction lies in transparency and openness. Traditional betting platforms are built around opacity, centralization, and control. Prediction markets, by contrast, are often built on public blockchains, where every trade, position change, market entry, and exit is recorded on-chain. Anyone can inspect these transactions in real time, including wallet activity and smart contract interactions. This openness enables behaviors and dynamics that are simply not possible on closed betting platforms. While the core concept is similar (betting on real world outcomes) prediction exchanges such as Polymarket and Kalshi create very different market dynamics.

- Regulation: The elephant in the room. The biggest unknown at the moment is regulation. At the time of writing, the largest exchanges are not available in all major countries, and Polymarket was banned from the US market for a significant period of time. Regulatory uncertainty remains a major constraint on growth and adoption.

- From hobby trading to professionalisation? Today, most participants are hobbyists, prosumers, and crypto traders. Institutional investors and hedge funds are largely absent. The open question is whether institutional investment firms will eventually adopt prediction markets. Historically, institutional participation has been a strong signal of market maturity, but we are not there yet.

- Are the dominant exchanges already established? Currently, two exchanges dominate the market: Polymarket and Kalshi. This raises the question of whether these are the long term winners. Are they the Amazon and the eBay of this ecosystem?

- Will they survive as standalone exchanges? Another open question is whether prediction markets will remain standalone products or become features embedded in larger platforms. It is possible that traditional betting companies like DraftKings, Unibet, or Winamax eventually offer similar products to their existing users. Or even stock market exchanges.

- Conclusion. Overall, this is still a nascent market. Despite billions of dollars being traded, it remains unclear how the stack will ultimately evolve and where long term value will concentrate. Is it a real trend or temporary hype?

Product and Technology Dynamics

- Exchanges: Polymarket and Kalshi, two different philosophies of prediction markets. When you just look at their homepage, Kalshi and Polymarket look very similar. But under the hood they differ in architecture and philosophy. For instance, Kalshi is a US regulated exchange operating under CFTC oversight, with USD rails, KYC requirements, and jurisdictional restrictions. This gives it institutional legitimacy, but it also slows market creation and constrains automation, since data access and execution are mediated through regulated infrastructure. Kalshi was originally built as a centralized, off-chain system, with matching, settlement, and accounts running on its own stack, and is only recently adding blockchain exposure through tokenized contracts on Solana. Polymarket, on the other hand, is crypto native and built directly on public blockchains (Polygon), where every trade, wallet, and position is on chain by default. This design enables permissionless access to data, rapid market creation, global participation, and widespread use of bots, making Polymarket behave more like an open financial protocol than a traditional exchange.

- Trading tools: The democratization of trading bots. Public equity markets are heavily automated (the majority of trades happening on stock markets are automated), so trade automation is not something new. However prediction markets differ fundamentally in visibility and access. Polymarket runs on public blockchains where every transaction, wallet, and position change is transparent, making it easy for anyone to build bots that monitor activity, react to information, or arbitrage markets with relatively low barriers. Traditional equity markets are also dominated by algorithmic trading but automation there is hidden behind fragmented exchanges, paid data feeds, brokers, and regulatory layers that obscure who trades and how. This openness lowers the barrier to entry for automation, enabling individuals and small teams to deploy bots using the same underlying data that professionals see. In that sense, prediction markets appear to democratize trading automation itself.

- Trading tools: From Telegram bots to mobile apps and web based terminals. Looking at the category of trading tools on the landscape, there is a wide range of product formats. Many products take the form of Telegram bots that allow users to trade directly from chat interfaces. Others are web based terminals, with a smaller number of mobile or desktop applications. Most of these tools are built by indie hackers and small teams, and many are still rough around the edges rather than fully polished products.

- API and middleware: Data access and intelligence as a service. One direct consequence of prediction market openness is the emergence of an ecosystem of APIs and middleware built on top of these exchanges. These tools make it easier for developers to build third party applications, ranging from trading bots to terminals and analytics products. Data APIs provide speed and scale, while some middleware offers higher level functionality as a service, such as simplified market access or even prediction as a service.

- Finance category: What could go wrong? Another interesting subcategory in terms of products, is finance focused tooling. This includes products that allow traders to create their own funds, like an AngelList for prediction markets, where successful traders can share their strategies and attract capital from regular users. It also includes tools for creating derivatives or collateralizing positions. Will things go wrong at some point? For sure, I’m 100% convinced of it 😅. But it’s also part of human history (and DNA some would bet).

Funding Environment

- Still too early for VC FOMO. Overall, I cannot say that we are seeing a large amount of VC activity or many funding rounds compared to other landscapes I have conducted recently. I believe the main reason is regulation and compliance, which make this space particularly risky for venture capital. Many of these companies operate on a thin regulatory line that most VCs prefer to avoid. This explains why the ecosystem is dominated by indie hackers and crypto community driven projects. Mainstream adoption (or lack of thereof) is probably another important factor.

- Layer 0 and 1: Infrastructure and exchanges are already heavily funded. The main exception is at the core of the stack, where several players are already well funded. Solana, Polygon, Polymarket, and Kalshi have all raised significant capital. In addition to traditional venture funding, token sales and ICOs have played a major role, especially for Solana and Polygon, enabling them to raise large amounts of capital through their own tokens. A key open question is whether this layer is already settled, with the main winners in place (I have the feeling that the answer is yes).

- Layer 2: Middleware and APIs. This layer has seen some venture activity, with examples such as Dome, Azuro, and Goldsky. However, we are still far from a wave of VC funding. If regulation becomes clearer and user adoption broadens, I think this is likely where the next round of venture investment will concentrate.

- Layer 3: Trading and analytics tools. This layer is largely the domain of indie hackers and small independent teams. There has been very little VC involvement, largely because user adoption is still limited and because active trading tools tend to be niche, prosumer oriented products that do not fit the typical VC model. I doubt that this layer will see significant venture interest, compared to the layers above.

- Conclusion: Overall, this ecosystem is still very early in its investment cycle. It is not even guaranteed that a large scale VC cycle will ever emerge if regulatory and compliance issues remain unresolved.

Exit and M&A Dynamics

As you can imagine, since we are still very early in the investment cycle, we are also very early in the M&A cycle.

- Exchanges: They are likely to acquire some startups over time, especially to expand functionality or integrate tooling. It’s not excluded that the exchanges themselves could become acquisition targets (by whom is another question).

- Middleware and APIs: These players are more likely to be acquired by existing trading platforms such as Robinhood, by institutional financial players, by larger data providers or the exchanges themselves. This is typically the layer where many small and medium acquisitions could happen.

- Trading bots and terminals: IMO This segment is likely to remain small in terms of M&A. Maybe some acquihire left and right, but I don’t see this category driving significant acquisitions (I might be wrong, time will tell).

Business Model

- Diverse models. Because prediction markets sit at the intersection of finance, crypto, and software, a wide range of business models coexist. These include trading fees, subscription based tools, API usage fees, and crypto native models based on tokens or protocol fees.

- Early monetization. The ecosystem is still very early, and many tools do not monetize yet. Exchanges already generate significant revenue and billions in transaction volume, but most products in adjacent layers remain in a pre monetization phase.

Value Capture

This section explores by whom and how value could be captured.

Using the four layer framework, here is how I think value will concentrate across the ecosystem.

- The biggest winners will be in the layers 1 and 0. I believe most of the value will accrue first to the exchanges themselves and then to their underlying infrastructure (Solana and Polygon). These are the central pieces of the ecosystem. Without them, there is no prediction market at all. If the market survives regulatory pressure and reaches mainstream adoption, these players are likely to capture the largest share of value.

- Layer 2: Middleware and APIs. The second most attractive layer, in my view, is Layer 2. These tools could capture meaningful value if adoption becomes widespread and regulation stabilizes. In that scenario, there will be strong demand for APIs and middleware from financial institutions, banks, investment firms, payment providers, as well as from media companies. Traditional financial markets eventually produced powerful data and infrastructure providers, Bloomberg being the canonical example, and a similar dynamic could emerge here.

- Layer 3: Applications. I’m personally not bullish on pure play trading tools and terminals. These products are likely to remain small, serving a niche prosumer audience and offering limited venture scale potential. Over time, I expect most of the value in this layer to be captured by established trading platforms such as Robinhood. These players already have distribution, can simplify the user experience, and can expose prediction markets to a much broader audience. If anything, they are likely to become the main distribution channel for prediction markets rather than the native tools built around them.

Prediction Markets 101: A Practical Q&A

What are Prediction Markets?

Prediction markets are platforms where people can bet on the outcome of future events by buying and selling simple contracts. Each contract represents a specific outcome, such as the result of an election or an economic decision, and its price reflects how likely the market believes that outcome is. The mechanism is similar to betting, but instead of fixed odds set by a bookmaker, prices move dynamically based on supply and demand. In practice, prediction markets turn collective opinions and information about the future into tradable prices.

How are markets/bets created on prediction markets?

On prediction markets, everything starts with a clearly defined question about a real world event, such as an election outcome, a policy decision, or a sports result. The market creator defines the possible outcomes and the rules for resolution, including the data source that will be used to determine the final result. Once the market is live, participants can buy or sell contracts linked to each outcome, with prices moving as people express their beliefs through trading.

On Kalshi, market creation is fully controlled by the platform. Kalshi defines, reviews, and launches markets itself, following strict regulatory requirements. Questions, outcomes, and resolution sources are all carefully specified in advance.

On Polymarket, markets are not created directly by end users either. Market creation is handled by Polymarket and its operators, but the process is much faster and more flexible than on regulated exchanges. The platform can spin up new markets quickly, cover a wider range of topics, and iterate rapidly. The openness comes from execution and data, not from permissionless market creation. Once an event is resolved using predefined sources, winning contracts pay out and losing ones expire worthless.

This distinction is important because Polymarket feels like a protocol, but market creation itself is still curated rather than fully permissionless.

What types of markets are typically available on Prediction platforms?

Prediction platforms usually group markets around a few recurring types of real world events.

- Political markets: Bets on elections, policy decisions, geopolitical events, or government actions. Examples include who will win an election, whether a law will pass, or how a country will act in a specific situation.

- Economic and macro markets: Markets tied to economic indicators and decisions, such as interest rate changes, inflation prints, recession calls, or central bank actions like Fed rate cuts.

- Sports markets: Bets on the outcome of sporting events, similar to traditional sports betting, but often framed as simple yes or no questions or win or lose outcomes.

- Crypto and financial markets: Markets focused on crypto prices, token launches, protocol events, ETF approvals, or major movements in financial markets.

- Technology and business markets: Bets related to company actions, product launches, acquisitions, IPOs, or milestones in the tech industry.

- Culture and internet markets: Lighter or viral markets about public figures, social media activity, or internet trends, often popular because they are easy to understand and trade.

Across all categories, the common point is that each market turns a clearly defined future event into a tradable contract with a clear resolution rule.

How does trading actually work on prediction markets?

On prediction markets, trading works through simple contracts that represent specific outcomes of an event. To participate, users need an account on the platform and, on blockchain based markets, a crypto wallet funded with the required currency (often stablecoins).

When a user believes an outcome is likely, they buy contracts for that outcome at the current market price. If they think it is unlikely, they can sell contracts instead. Prices move continuously as people trade, reflecting changing beliefs and new information.

Importantly, users do not need to wait until the event is resolved to exit a position (it’s not like on traditional betting platforms). Contracts can be sold at any time before resolution, allowing traders to lock in profits or cut losses as prices move. For example, if I believed early on that candidate X would win the next election (and bought contracts about it), and if closer to the voting date its chances increased and the price went up, I could sell my position before the election takes place and cash out profits.

When the event is officially resolved, winning contracts pay out a fixed amount, while losing contracts expire worthless. In practice, this makes prediction markets feel closer to trading than to traditional betting, with liquidity, price movement, and timing playing a central role.

How do Polymarket and Kalshi differ?

When you look at Kalshi and Polymarket websites, you have the impression that both platforms are similar. But they do differ under the surface and it shapes who can use them, how capital moves, and what kind of market emerges.

Kalshi is built as a fully regulated financial exchange in the United States. It operates under CFTC oversight, uses USD rails, and enforces KYC and jurisdictional restrictions. This gives Kalshi a stronger legitimacy with institutions, media partners, and corporate users. But that also constrains the product. For example, market creation is slower, assets are tightly defined, and automation is more limited because access, data, and execution are mediated through regulated infrastructure.

Polymarket is built as a crypto native, on-chain marketplace. It runs on public blockchains, uses stablecoins, and exposes every trade, wallet, and position publicly. Anyone can read the data, build bots, copy strategies, or arbitrage markets without permission. This openness favors rapid market creation, global participation, and a heavy presence of automated traders. The product looks similar, but the it behaves more like an open financial protocol than a traditional exchange.

What’s also interesting is that Kalshi was not originally built as a public blockchain native platform the way Polymarket is. It started as a centralized, regulated exchange for event contracts that are traded off chain under oversight by the U.S. Commodity Futures Trading Commission (CFTC). The matching, pricing, user accounts, and settlement logic all run on Kalshi’s own infrastructure rather than directly on a blockchain ledger. That being said, Kalshi is increasingly integrating blockchain technology by tokenizing its prediction contracts on networks like Solana and expanding access via chains like TRON.

On the other hand, Polymarket’s markets are built directly on public blockchains (Polygon), so every trade and position is on-chain by default.

Are prediction markets always efficient, and why do price imbalances exist?

Prediction markets are not perfectly efficient, especially in their early stages, and that is part of their nature. When a market is first created, there is often little liquidity and no well established price, so early trades can be noisy, biased, or driven by a small number of participants. Prices gradually improve as more people enter, bring information, and trade against each other. Over time, the market tends to converge toward a more accurate probability, but this process is uneven and depends heavily on participation.

These early inefficiencies create opportunities for trading strategies. Some traders focus on entering markets very early to benefit from mispriced contracts. Others look for temporary imbalances caused by news delays, emotional reactions, or low liquidity. Because prediction markets aggregate beliefs rather than rely on a central price setter, inefficiencies are not a bug but a feature. They are the mechanism through which information gets incorporated into prices.